travelview // Shutterstock

The housing âsingles taxâ: Why married buyers are coming out ahead

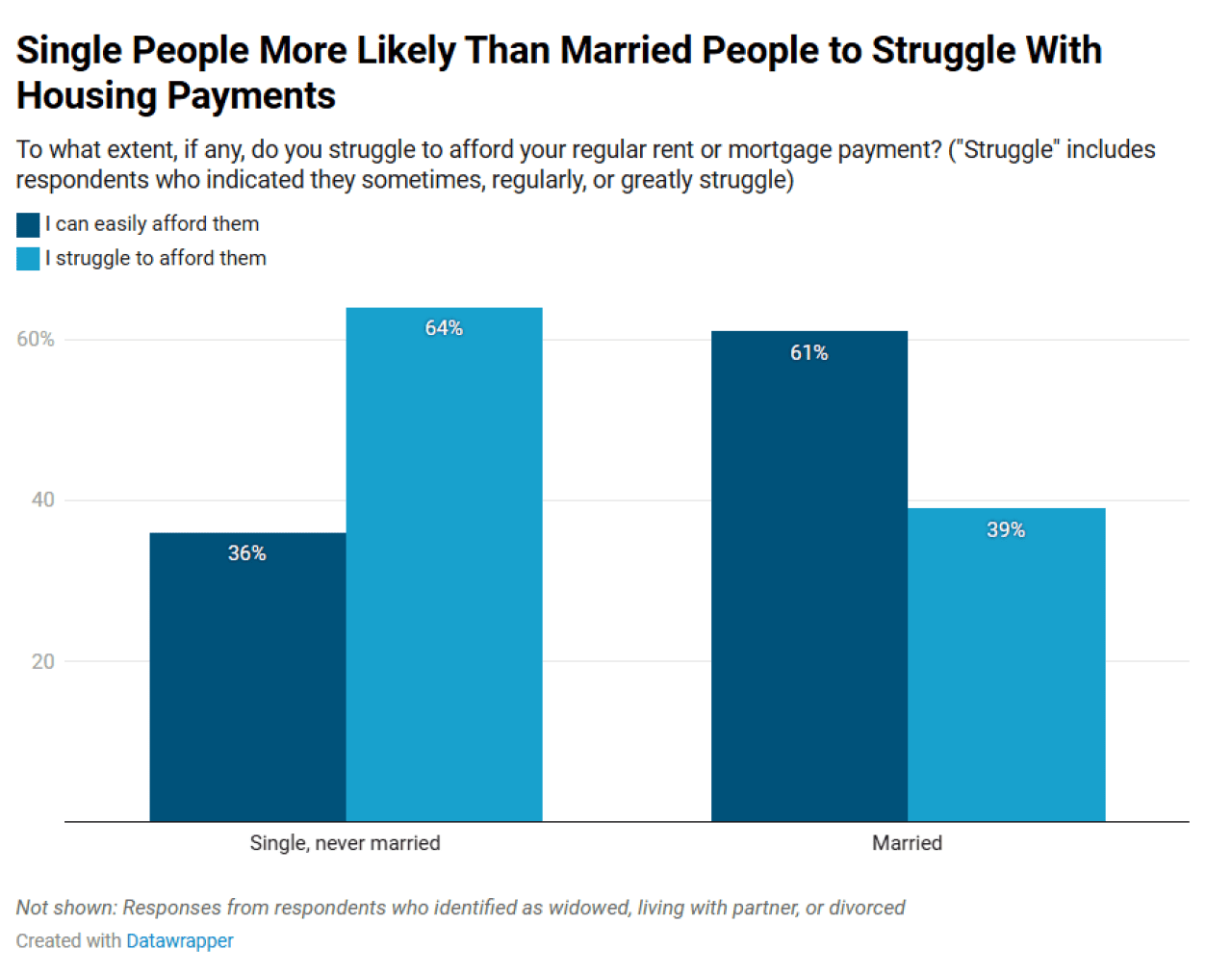

Housing has never been so expensiveâand single people are feeling the strain the most. Nearly two-thirds (64%) of single people struggle to afford their regular rent or mortgage payments, compared with 39% of married people, according to a recent Redfin Real Estate survey.

Redfin Real Estate

Why single people struggle to afford housing

Along with ubiquitous rising housing costs, single people have a harder time affording housing than married people for four key reasons:

- Household income is lower for single people. Single people are stuck paying prices much better suited to a double-income on a single-income budget. 48% of single survey respondents reported earning a household income of less than $50,000 per year, compared with just 9% of married people. On the flip side, married people are three times more likely than single people to earn household incomes between $100,000 and $500,000 (62% versus 21%).

- Single people face more financial disadvantages. Married couples receive tax benefits that single people donât get. And in many cases, married couples split the cost of other expenses like groceries, gas, and childcare, so each individual has a smaller financial burden.

- Single people tend to be younger than married people. That means theyâre earlier in their careers and havenât yet hit their earning peakâand they have had less time to build savings. Additionally, many Gen Zers and millennials are still paying off student debt. A recent Redfin report on homeownership by generation delves deeper into reasons why it is more difficult for young Americans than older Americans to buy homes.

- Zoning policies favor married couples. A majority of U.S. residential property is zoned for single-family housing, which tends to be less affordable for single people. Today, married couples make up a smaller share of U.S. households than they used to. To better meet Americans where theyâre at, Redfin economists suggest that officials could consider zoning for ADUs and single-room housing, and cutting red tape to make it easier to build apartment complexes and condos.

Single people pay the most in Washington D.C. and the Bay Area

Washington D.C. has among the highest populations of single people in the country, accounting for more than half of its adult population.

The typical condo in the D.C. metro area costs $379,000. A buyerâs monthly payment would be $2,974, using current mortgage rates and assuming a $566 HOA fee. A single person living alone would cover the whole cost themselves, while a married or cohabitating couple may split the cost and pay $1,487 each. Annually, a single person would pay a double-digit âsingles taxâ of $17,844.

Say youâre single and living alone in San Francisco, one of the most expensive housing markets in the U.S. The typical condo there costs $980,000, with a monthly payment of $6,950 (todayâs mortgage rates and a $724 HOA fee, the local median). A single person would pay that alone rather than paying half ($3,475), giving San Francisco a âsingles taxâ of $41,700.

Lack of affordability is keeping single people from moving

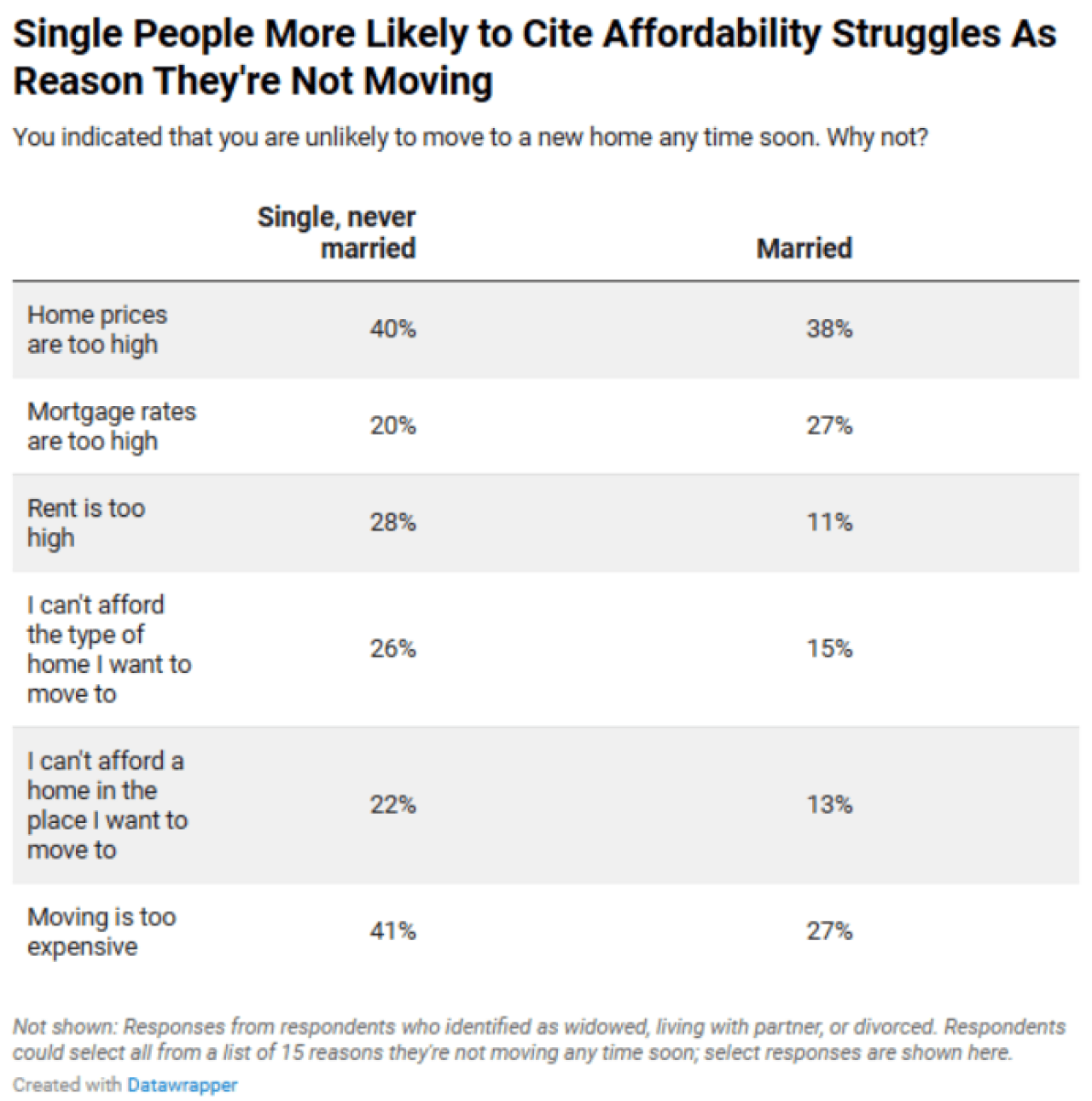

Single Americans are more likely than their married counterparts to cite lack of affordability as a reason they wonât be moving anytime soon.

Single people are nearly twice as likely as married people to say theyâre not moving because they canât afford the type of home they want to move to. More than two in five (41%) single people say theyâre not moving because moving is too expensive, compared with 27% of married couples.

Redfin Real Estate

Everyone is struggling to afford housing

Single people are bearing the brunt of the affordability crisis, but everyone is struggling. One-third of all homeownersâsingle or otherwiseâstruggle to afford monthly payments; for renters, this share jumps to 49%.

Affordability has plunged in the past three years due to a combination of skyrocketing sale prices and mortgage rates. Home-sale prices have risen nearly 50% since before the pandemic, while rental prices have risen about 20%. Wages have increased, but not as much as housing costs. Add in rising costs for just about all other day-to-day expensesâand unprecedented economic uncertaintyâand millions of families are left with little cushion.

The bright side is that affordability slowly improved in 2025, as mortgage rates fell and sale price and rent growth slowed. As of December 2025, the typical homeowner had to spend $111,252 to buy a typical U.S. home, down from the $122,000 peak six months prior. The typical renter had to spend $76,000, down from $77,000 earlier in the year.

Redfin economists predict that affordability will continue to improve in 2026 and beyond, marking the beginning of a recovery for the housing market as wages rise faster than home prices for a prolonged period of time.

This story was produced by Redfin Real Estate and reviewed and distributed by Stacker.

![]()